Currency, Commodity, Bitcoin

Money is fascinating. What’s more fascinating is the value of money, a quality so enigmatic that one can hardly point to a single definitive reason why the Canadian dollar is currently valued at $0.98 USD. Personally I use USD because I live in the United States. Sure, there are currency exchanges where I could purchase foreign dollars and I’m sure my bank would be more than happy to turn some of my American funds into something more exotic for a fee, but being the modest earner that I am I tend to stick to the greenbacks my paycheck provides.

Let’s pretend for a moment, though, that I have suddenly become distrustful of the government. I can put my faith in our neighbors to the North and convert all of my liquid assets to CAD, but there won’t be anywhere for me to spend them in the neighborhood. Even if I could, why should I have to trust another mortal, fallible group of humans just like me? Why can’t currency just be currency? Whether spurned by the recent financial crisis in Cyprus or by increasingly subversive and paranoid citizens of the world, Bitcoin’s meteoric rise in 2013 is one of the most interesting phenomena to enter our collective consciousness in recent memory. While its status as a legitimate store of value is still tenuous, the currency or commodity known as Bitcoin has already had a monumental impact on our relationship to money and may usher in a new era of democratic capitalism driven by leaders in technology.

Why Bitcoin Matters for Software

On the surface, Bitcoin has little to do with the software industry. There is no singular Bitcoin program or app, it doesn’t have a single team in charge of operations, and its goal isn’t to make money but to mint it. If you’re still scratching your head wondering what the hell a Bitcoin is, keep calm and read on, but for now know that the world around you is changing. As a small first step, tech companies like Expensify, Reddit, Namecheap, and the world’s most used CMS, WordPress, have already begun accepting Bitcoin as payment. This is more than a mere stunt by CEOs to make themselves seem hip. Leaders in tech are recognizing that Bitcoin has the potential to loosen the grip that governments and financial organizations like the IMF currently hold on worldwide banking:

‘Bitcoin is perfect for international transfers,’ Expensify CEO David Barrett told VentureBeat. ‘It’s secure, instantaneous, and totally free. We support PayPal, but it is expensive. A four percent charge on a large reimbursement can really add up.’

Not only is Bitcoin useful in the present for sending money around the globe, but Boost VC founder Adam Draper, “recently announced that the team would be focusing on Bitcoin-focused startups for its summer class,” meaning that investors see potential in the future of digital currency. This is not to say that betting on Bitcoin is a guaranteed win, far from it, but there’s currently nothing like it and early adopters are cashing in.

Graph of Bitcoin trading price 2/15/2013-4/15/2013 at MtGox.com by BitcoinCharts.com

What is Bitcoin?

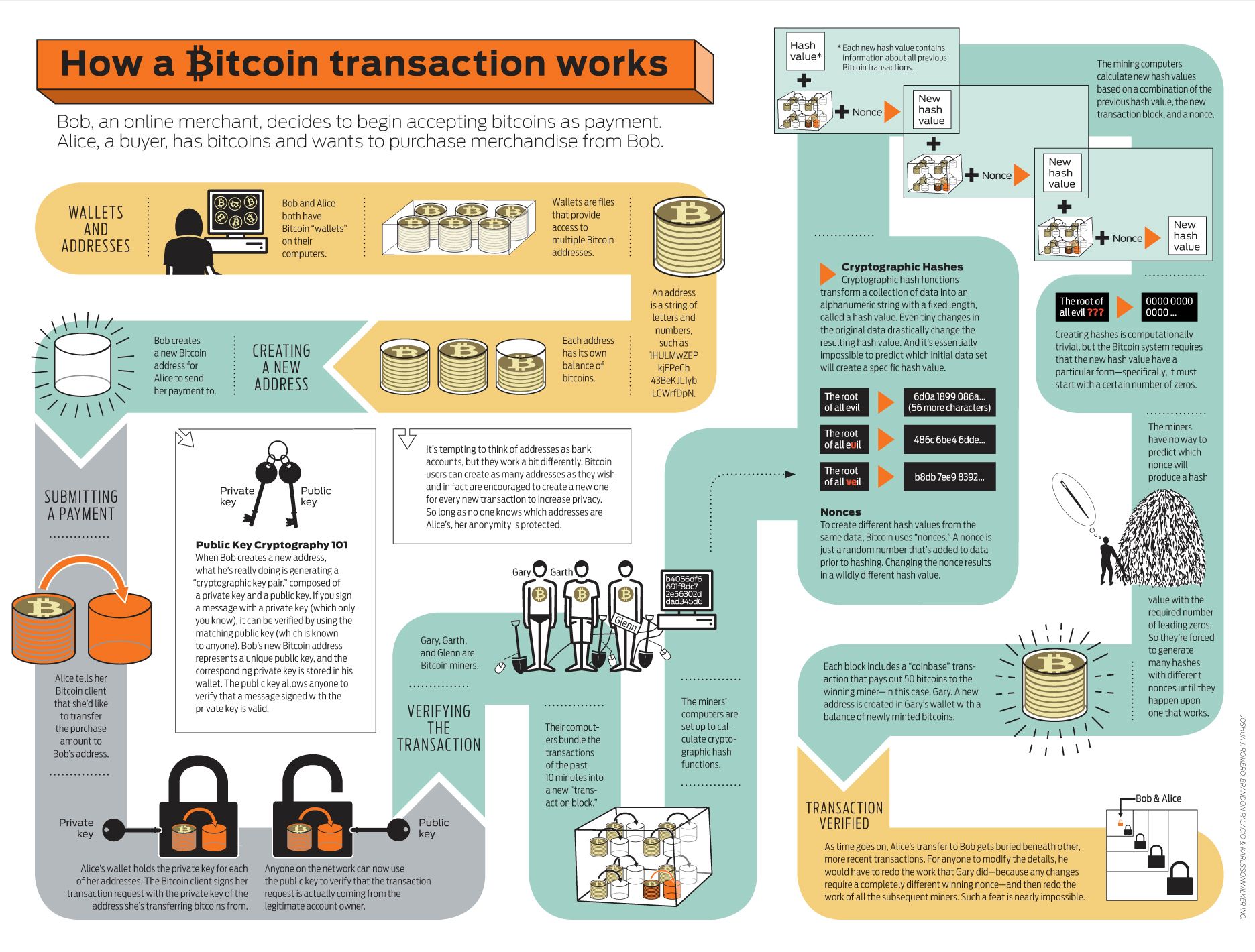

Understanding why there’s such a frenzy of attention around the implications of Bitcoin requires dedicating a little bit of time to developing an understanding how Bitcoin works in a technical sense. To borrow from Timothy B. Lee who cites Nikolei Kaplanov, there are essentially three types of users operating within the Bitcoin sphere at any given time.

The first are ordinary users who may or may not have any technical savvy and can willingly buy, sell, or exchange Bitcoins on the open (or black) market. These people, according to Kaplanov, are completely exempt from legal consequences as long as the goods being exchanged are legal in the countries they’re being sent to and from. In this sense, the end user of Bitcoin is very similar to someone who purchases in-game currency while playing FarmVille and exchanges that currency for goods, though in Facebook’s case the goods are digital.

The next group, called miners, begin to add complexity to the question of Bitcoin’s legal status. First, the term ‘mining’ is used for lack of a better word to describe a process of solving complex mathematical equations using computers in a peer-to-peer network. When Bitcoin began in 2009, it was predetermined that there would only ever be 21 million Bitcoins and that this quantity would be reached in 2140. The creation of new Bitcoins then is not a matter of when but who. Who will solve the problems required to mint new Bitcoins? By its design, “the first half of the Bitcoin supply was created in the first four years, the entire second half however will take another 127 years,” and, “the rate at which new Bitcoins are mined [is halved] every 4 years.” This still doesn’t explain how mining occurs, though.

All Bitcoin transactions ever made are stored in a publicly available log called the blockchain. “Mining” is simply contributing one’s computer processing power toward the verification of new transactions in the blockchain. Individuals (or more often, extremely large groups called pools) that help build the blockchain are rewarded at random with newly minted Bitcoins. In the early days of Bitcoin, modest processing power might have provided a decent return but the diminished gains of today mean that even as part of a pool your odds of receiving significant remuneration by mining from your personal computer are slim to none. I won’t be delving any deeper into the technical aspects of mining here, but for those that are curious, take a look at Vice’s rundown of Bitcoin mining and the hardware that has been developed to support it.

Image by Joshua J. Romero, Brandon Palacio & Karlssonwilker Inc.

To return to Kaplanov and Lee, despite that miners are, “facilitating the transfer of funds from one Bitcoin user to another,” as Lee puts it; Kaplanov does not think they are legally culpable. The problem with indicting a miner is that they don’t possess the information that the government would indict them for in the first place, which is to say the only information they possess is the publicly-available blockchain and, “the pseudonymous Bitcoin addresses associated with each transaction,” that comprise it. Not only that, but as mining becomes a group effort in the form of pools, identifying an individual as the sole facilitator of a transaction becomes practically impossible.

The third piece of the puzzle, and the group that has had the most legal trouble, are the exchanges. Much like regular currency exchanges, their only purpose is to convert Bitcoins to traditional currency and vice versa. Because these organizations are “money-transmitting services” they are subject to local laws and governance which have forced some exchanges in the United States to close. As Lee notes, the largest Bitcoin exchange in the world, Mt.Gox, is based in Japan.

Arguments Against

To provide a complete picture of Bitcoin skepticism, I will be referencing arguments from the work of Timothy B. Lee and Alec Liu. This is the same Timothy Lee responsible for writing the summary of Kaplanov’s work from 2012 cited above, but keep in mind that the price of Bitcoin did not begin to rise rapidly until February of this year.

Insurance

The primary criticism levied against Bitcoin by many in the financial world is that it lacks the fundamental stability that centralized administration provides. Unlike traditional forms of payment (cash, credit card) that are insured either by governments or corporations, Bitcoins are held in uninsured digital wallets either locally or by online wallet services, either of which is vulnerable to a security breach. Furthermore, because Bitcoin has no official leader, technical difficulties fall to whoever is there to fix them pro bono.

Monopoly

Despite that there are 127 years of Bitcoin mining left; the fact that the number of Bitcoins is finite by design means that there is potential for a monopoly to occur. If this was the case and the monopoly holder was to sell a few million Bitcoins at once, the market for Bitcoin would likely destabilize. Fortunately for proponents, more than half of the 21 million Bitcoins that will eventually exist have already been mined which means that the only person who realistically stands a chance of reaching a monopoly is Yifu Guo, co-founder of Chinese Bitcoin mining hardware manufacturer Avalon. Guo, however, has stated that he has no plans to pursue a monopoly and that profit has never been his goal.

Yifu Guo, Co-Founder of Avalon. Image by Vice.

Scale

Another potential roadblock on the path to Bitcoin’s success is its cumbersome method of recordkeeping. Because the blockchain contains a record of all transactions, its size continues to grow and requires that a larger file be common among all peers. This problem is less a shortcoming of Bitcoin and more an acknowledgement that Bitcoin would likely struggle to take the place of Visa or American Express.

Sanction

Perhaps the most interesting extrapolation of Bitcoin’s future is that like all good things it will eventually be changed, that its corners will be rounded before it is considered legitimate in the eyes of authorities around the world. Bitcoin’s current legal status is a Catch-22: its greatest asset is its freedom from restrictions as a not-quite-currency and yet there is demand for Bitcoin to be accepted as payment at chain retailers as consumers whine about the dearth of Bitcoin outlets. The situation is complicated by the threat of impending sanction by the United States, though if its attempts to stifle BitTorrent have taught us anything it’s that you can’t kill the hydra by cutting off a single head.

Rebuttal

The first beacon of Bitcoin’s shiny new legitimacy is the Bitcoin Foundation led by Gavin Andresen. Though Andresen is not the group’s official leader, he is the face of the organization and its Chief Scientist. The group’s goals are simple: standardize Bitcoin infrastructure, make Bitcoin as or more secure than traditional currency, and promote Bitcoin by, “Allowing the community to speak through a single source.”

But why are so many well-to-do American men interested in legitimizing Bitcoin? One can only assume life, liberty, and happiness, which is exactly why Bitcoin has become so popular in the European Union of late. It’s been hard to ignore the crisis currently playing out in Cyprus, the Mediterranean island state and the latest EU member to face financial collapse, but what you may not have heard is why Bitcoin is thriving there. European officials under pressure to maintain their union after the bailout of Greece decided to freeze Cypriot bank accounts and withdraw a minimum of 6.75%. The problem is, this breaks an EU promise to protect insured deposits on the eve of potential crises in Italy, Portugal and Spain. As a result, concerned citizens across Europe are moving their funds, at least partially, into Bitcoin.

Prototype of a Bitcoin ATM by BitcoinATM.com

Yes, it may be volatile. Yes, you may lose all of your money tomorrow. No, nobody can officially take it away from you. This seems to be enough of a selling point for EU citizens as their governments are losing an essential element in the value of their currency: trust. To quote Bloomberg’s Paul Ford:

Trust is hard to earn; verifying transactions is a brutal problem, which is why PayPal locks down your account when there’s too much money flowing into it. Creating trust is traditionally the work of federal governments and branding agencies. Trust is also an easy thing to squander. Just close a beloved service, à la Google Reader. Or allow your banks to fail, causing an entire country to suddenly realize that the value of their deposits, the fundamental integrity of their financial selves, was arbitrary all along.

Ford ends his article with a bombshell: “Bitcoin isn’t tied to any commodity—besides trust.” Finally, the currency which escapes all definition has a metric, and it’s flexible.

Currency, Commodity, Bitcoin

So far we have explored how Bitcoin works, its potential problems and their solutions, and why it has enjoyed such rapid growth in recent months. In an article by Felix Salmon, he presents a vision of Bitcoin’s future that seems eerily poised to come true. Whether Salmon’s predictions are prescient we may not know for some time, but to ignore them would be to ignore a phenomenon that now has a total value near $1 billion.

Adding to the mystery of Bitcoin is its apocryphal founder, a Japanese citizen by the name of Satoshi Nakamoto who has since released statements but has never been seen or heard. Salmon notes that Nakamoto’s fundamental belief that, “The root problem with conventional currency is all the trust that’s required to make it work,” is precisely the message that financial maven Warren Buffett delivered to shareholders in 2012: “Investments that are denominated in a given currency…are thought of as ‘safe.’ In truth they are among the most dangerous of assets.”

As Salmon writes, “If you hold dollars, you’re trusting the US government to not destroy your wealth. Bitcoin, by contract, is based on mistrust—it’s specifically designed so that it’s every man for himself.” Salmon’s claim is not a hypothesis but a truth of Bitcoin’s design. Bitcoins subvert currency because they aren’t currency. Bitcoins are immune to seizure or freezing, operate like cash without the requirement of physical presence, and in this sense, are more accurately described as a commodity.

Tony Gallippi, founder of payment gateway Bitpay.com, agrees. In an interview with Business Insider, Gallippi explains that the only thing holding Bitcoin back is its price, which he believes will continue to rise:

There’s volatility now, the market has it undervalued, so people [who are] trying to do larger transactions, the market can’t handle it. But if there are $10 billion worth of Bitcoins in the market, it’s not really going to move on market volatility.

As for security concerns and the threat of government sanction, Gallippi sees the number of attacks falling as incentive to keep the system secure grows and that governments will eventually come to treat gateways like Bitpay as payment processors similar to casinos distributing chips.

Regardless of Bitcoin’s eventual classification as a currency, commodity, or both, it persists. Since its inception, the internet has forced us to shake off our old notions of what is possible. Phone calls used to require phones. Music used to require file storage. Currency used to require banks. The beauty of Bitcoin is that it has no purpose but to exist as a store of value. Yifu Guo put it best when he said:

Bitcoin’s core features–ease of transfer and production without middlemen–will always give it value. That’s why we don’t really care about its exchange rate. We don’t look at it like a stock, we look at it like technology. It’s a platform. How can we take Bitcoin’s strengths, its cryptography, its decentralization, and how do we utilize and leverage this model? Whatever business you’re running right now, add Bitcoin to the equation and you’ll see instant profits.

Graph of gold trading price 2004-2013 by Monex.com

Want to read more insider-perspective posts on bitcoin and other trends in the financial industry? Browse our entire archive of blog posts on news from the software industry by visiting the News and Trends section of the Business-Software.com blog.

- Top Expert

Michael Tauscher

Expert in Accounting, CMS, CRM, and Analytics